- Blogs, News articles

Key superannuation thresholds set to be indexed

While it had previously been widely anticipated, the recent release of Consumer Price Index (CPI) and Average Weekly Earnings (AWOTE) data from the Australian Bureau of Statistics (ABS) provides confirmation that key superannuation thresholds are set to increase from 1 July 2026.

Transfer Balance Cap (TBC)

From 1 July 2026, the General TBC is set to increase to $2,100,000 (an increase from $2,000,000).

This increase follows previous increases which took place on 1 July 2021 (to $1,700,000), 1 July 2023 (to $1,900,000), and 1 July 2025 (to $2,000,000).

Individuals who, on 1 July 2026, are yet to commence a retirement phase income stream will receive the full benefit of this increase when they first commence a retirement phase income stream.

However, for others, due to the proportional indexation that is applied to a member’s Personal TBC, not everyone will benefit by the same amount. Any increase to their Personal TBC will involve a complicated calculation – based broadly on how much they have previously used to commence a retirement phase pension account.

Unfortunately, those who have already fully utilised their personal TBC before 1 July 2026, will not benefit at all from this increase to the General TBC.

Important considerations

Some members, currently considering the commencement of their first retirement phase income stream, may benefit from deferring until 1 July 2026 to lock in a larger Personal TBC.

At the same time, members currently receiving a Transition to Retirement Income Stream (TRIS) should remain vigilant and ensure that their TRIS doesn’t inadvertently convert to a retirement phase pension before 1 July 2026 – as this will impact the size of their Personal TBC.

Contributions caps

From 1 July 2026, the Concessional Contribution (CC) cap will increase to $32,500 (an increase from $30,000).

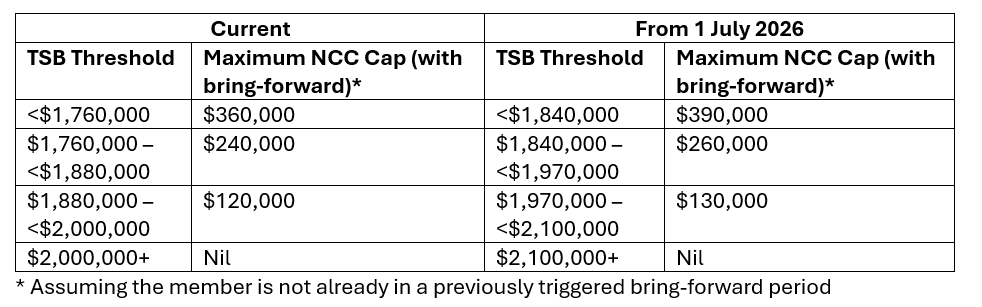

Further, as the Non-Concessional Contribution (NCC) cap is calculated as four times the CC, the NCC cap is also set to increase to $130,000 (an increase from $120,000).

Importantly, when combined with the abovementioned increase to the General TBC, the thresholds relevant for determining the point at which an individual is able to trigger a NCC bring-forward period, and the point at which a member’s NCC cap is reduced to zero, are also set to change.

Written by Fabian Bussoletti, Technical Manager, SMSF Association

Important considerations

Obviously the increase to the contribution caps will enable larger contributions to be made (where an individual is eligible to do so).

For those who may have previously been locked out of making NCCs, due to their TSB exceeding the maximum threshold ($2,000,000 for the 2025-26 year), the increase in this cut-off point to $2,100,000 may provide a new opportunity for additional NCC contributions to be made in 2026-27.

However, for those who are already in a bring-forward period, there will be no change to the amount that they originally locked in, nor to the time remaining until the expiry of their existing bring-forward period.

As such, careful consideration is required before triggering a bring-forward period between now and 1 July 2026.

Of course, the above assumes that there is no change to legislation (including any potential Federal Budget announcement) in the prevailing period.