- Go-To Guide

- Income streams, Setup and management

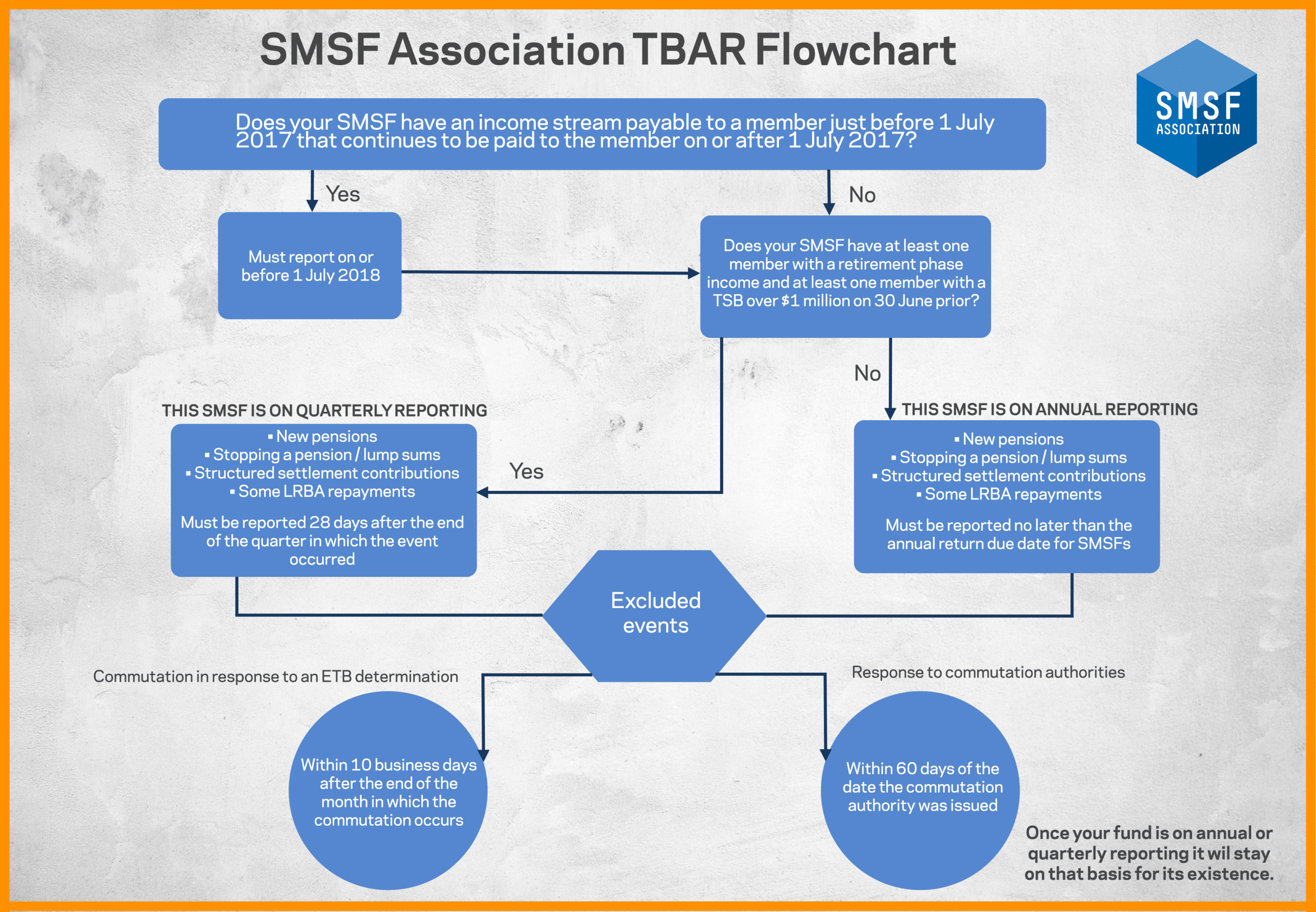

The SMSF Association has compiled a new Go-To Guide on TBAR (Transfer Balance Account Reporting) to ensure you are confident in your understanding of the Transfer Balance Cap and event-based reporting framework.

Reporting requirements commence for all SMSFs on or before 1 July 2018 where an individual has a retirement phase income stream at 30 June 2017 that continues to be paid to an individual on or after 1 July 2017.

As event-based reporting is a significant shift in SMSF administration processes, it is essential SMSF Specialists, administrators and advisors understand the event-based reporting framework and get it right.

Go-To Guides are comprehensive technical documents which contain practical guidance, an interactive checklist, detailed case studies and a white label document that can assist you in communicating with your clients on how event-based reporting may affect them and their SMSF.

{kind=link}

At the time of publishing, the contents of this resource were accurate and correct.

Disclaimer: Technical Papers contain factual information only and are prepared without considering particular objectives, financial circumstances and needs. The information provided is not a substitute for legal, tax and financial product advice. The information contained in this document does not constitute advice given by the SMSF Association to you. If you rely on this information yourself or to provide advice to other persons, then you do so at your own risk. The SMSF Association is not licensed to provide financial product advice, legal advice or taxation advice. We recommend that you seek appropriate professional advice before relying upon the information in this technical paper. While the SMSF Association believes that the information provided is accurate, no warranty is given as to its accuracy and persons who rely on this information do so at their own risk. The information provided in this paper is not considered financial advice for the purposes of the Corporations Act 2001. © SMSF Association